FloatMe sounds like a lifeline — until you hit the $50 advance cap and realize it barely covers a tank of gas. Millions of users have downloaded the app hoping for real emergency relief, only to find themselves denied outright because their direct deposit doesn’t qualify, or quietly paying $3.99 a month for access to an advance that doesn’t move the needle. Gig workers and freelancers get hit hardest: FloatMe’s eligibility requirements are built around traditional W-2 employment, leaving a huge chunk of the workforce locked out entirely.

The frustration is legitimate. A subscription fee that outpaces the value of the advance — when calculated as an effective APR — is a bad deal, full stop. And there are better options out there, several of them free.

Below are the 10 best apps like FloatMe, ranked by advance limits, true cost, transfer speed, and whether they work for non-traditional income earners. A full comparison table makes the right choice obvious at a glance.

Why Users Look for FloatMe Alternatives

FloatMe’s core limitations hit hardest exactly when you need cash most. The $50 advance ceiling, a mandatory subscription fee, and strict eligibility rules push a significant portion of users — especially gig workers and freelancers — toward competing apps before they ever see a dollar.

FloatMe’s $50 Advance Cap

Fifty dollars doesn’t cover much. A tank of gas in most states runs $50 to $70; a single utility bill or a week of groceries easily doubles that. FloatMe caps every advance at $50, and many users report being approved for far less — sometimes $10 or $20 — based on their account activity.

For a genuine financial shortfall, that ceiling isn’t a safety net. It’s a speed bump.

Subscription Fees and Hidden Costs

FloatMe charges $3.99 per month just to access its advance feature. Borrow the maximum $50 and repay it within two weeks, and that subscription fee alone represents an effective annualized cost of roughly 96% APR — before any express transfer fees. Several competing apps offer free tiers with no subscription required at all.

The math simply doesn’t favor FloatMe for small, short-term advances.

Eligibility Restrictions That Lock Users Out

FloatMe requires a qualifying direct deposit from an employer — a condition that disqualifies freelancers, gig workers, and anyone paid via PayPal, Venmo, or marketplace platforms like DoorDash and similar delivery apps or Upwork. New bank accounts and irregular income patterns trigger automatic denials as well.

Gig workers represent a disproportionately large share of people searching for apps like FloatMe, yet FloatMe’s eligibility model was built for traditional W-2 employees. That mismatch is the single biggest driver pushing users toward more flexible alternatives.

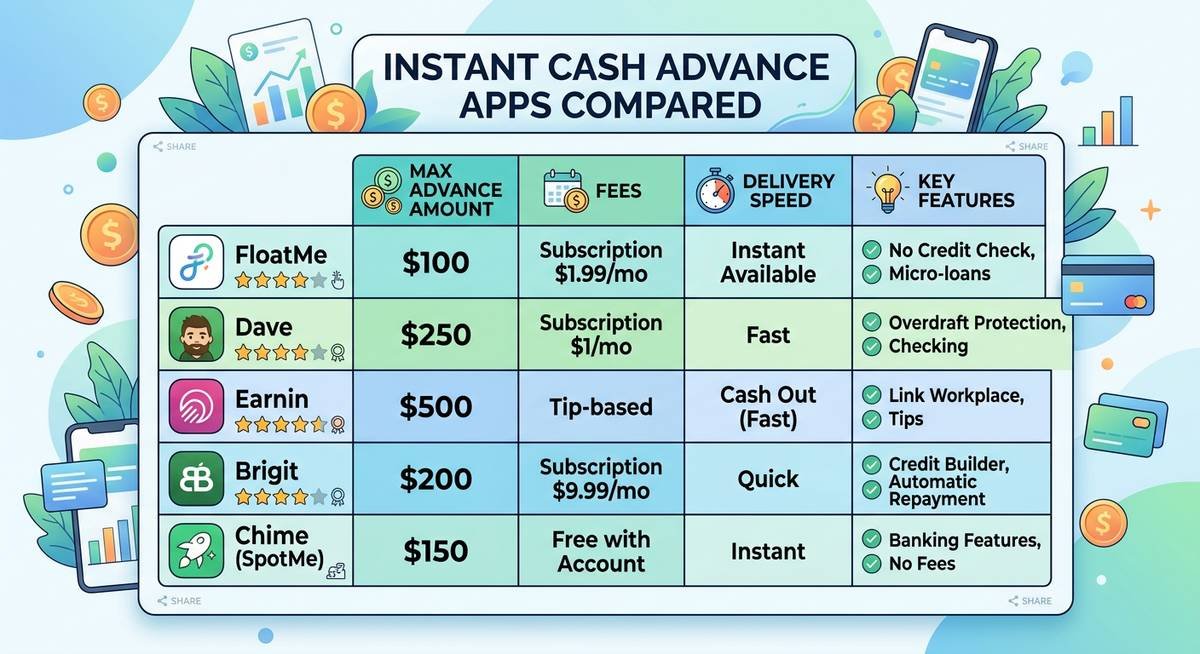

Top 10 Apps Like FloatMe at a Glance

These ten FloatMe alternatives range from completely free options like Gerald to subscription-based platforms like Brigit. Advance limits, transfer fees, and income requirements vary dramatically across the board. Knowing where each app stands on six key metrics before downloading saves time and avoids surprises — especially for gig workers who may get rejected at signup.

How to Read This Comparison Table

Each app is measured across six columns. Max advance is the ceiling under ideal conditions — real limits are often lower for new users. Subscription cost is the monthly fee to access borrowing features. Instant transfer fee is the separate charge to get money in minutes rather than days. Credit check flags whether a hard inquiry is involved. Income type distinguishes apps requiring W-2 direct deposits from those accepting gig, freelance, or irregular income. Minimum eligibility captures the most common reason applications get denied.

Full Comparison Table

| App | Max Advance | Monthly Fee | Instant Fee | Credit Check | Income Type | Key Eligibility |

|---|---|---|---|---|---|---|

| EarnIn | $750/pay period | $0 | $3.99 | No | W-2 (location/timesheet verified) | Consistent direct deposit + employer verification |

| Dave | $500 | $1 | $3 to $15 | No | W-2 preferred; Dave bank required for top limits | Dave checking account + spending history |

| Brigit | $250 | $9.99 | $0 (included) | No | W-2; regular direct deposit | Paid plan required for any advance |

| Chime SpotMe | $200 | $0 | $0 | No | W-2; Chime account required | $200+/month direct deposit into Chime |

| MoneyLion | $500 | $0 to $19.99 | $0 to $8.99 | No | W-2 or gig (RoarMoney account) | RoarMoney account for highest limits |

| Albert | $250 | $0 to $14.99 | $6.99 | No | W-2 or gig (variable approval) | Linked bank account with recurring deposits |

| Klover | $200 | $0 | $0 to $3.99 | No | W-2 or gig | Linked bank account with deposit history |

| Cleo | $250 | $5.99 | $0 (included) | No | W-2 or gig (connected bank) | Cleo Plus/Builder subscription required |

| Payactiv | $500 (earned wages) | $0 | $0 to $3.49 | No | W-2 (employer must partner with Payactiv) | Employer enrollment in Payactiv program |

| Gerald | $100 | $0 | $0 | No | W-2 or gig | Bank account linked; buy a Gerald product first |

None of these apps run a hard credit check, meaning your credit score stays untouched regardless of which you choose. The real differentiators are advance ceiling, total cost, and whether the app accepts non-traditional income.

The 10 Best FloatMe Alternatives Reviewed

Each app below is evaluated on advance ceiling, real cost, speed, and at least one honest limitation that competitors rarely mention. Advance limits listed are maximums — most new users start lower.

1. EarnIn

EarnIn allows access to up to $750 per pay period with zero mandatory fees — the tip model is genuinely optional, according to EarnIn’s terms. For workers living paycheck to paycheck, that ceiling is roughly 15x what FloatMe offers. The Lightning Speed feature delivers funds in minutes for $3.99.

The catch: EarnIn requires either consistent GPS location data tied to a physical workplace or verifiable timesheets. Remote workers and gig earners with irregular schedules are effectively excluded. The app also reduces available amounts if it detects overdraft risk in the linked bank account.

2. Dave

Dave’s ExtraCash feature advances up to $500 at just $1/month — one of the lowest recurring costs in the category. Free standard transfers arrive in one to three business days. Express delivery runs $3 to $15 depending on the advance amount.

Eligibility is heavily weighted toward spending history inside Dave’s own banking product. New users who sign up expecting the full $500 typically qualify for $25 to $75 on their first advance. Building up to the ceiling takes months of consistent deposits into the Dave checking account.

3. Brigit

Brigit advances up to $250 and pairs it with genuinely useful budgeting and credit-building tools. Pricing is transparent: $9.99/month for the Plus plan that unlocks cash advances, with instant delivery included at no extra cost.

The effective cost is steep. Paying roughly $120/year to access a $250 advance produces an annualized cost well above traditional lending rates. There is no free borrowing tier whatsoever, which disqualifies Brigit for anyone who only needs occasional advances. For frequent borrowers who also use the budgeting features, the value proposition improves.

4. Chime SpotMe

Chime SpotMe covers overdrafts up to $200 with zero fees — no subscription, no express charge, no tip prompt. For users already banking with Chime, it’s the cleanest value proposition on the list.

The limitation is absolute: SpotMe only functions within the Chime ecosystem. A qualifying direct deposit of at least $200/month is required, and Chime must be the primary bank account. Anyone unwilling to switch banks gets nothing from this feature. SpotMe limits also start low (often $20) and increase based on deposit history.

5. MoneyLion

MoneyLion’s Instacash feature advances up to $500 with a free base tier available for smaller amounts. The RoarMoney banking account integration unlocks higher limits and faster transfers without additional fees.

Reaching the $500 ceiling requires a Credit Builder Plus membership at $19.99/month, which transforms a seemingly free product into one of the more expensive options available. MoneyLion is best suited for users who want the full financial platform — investing, credit building, and banking — rather than just a standalone cash advance.

6. Albert

Albert offers cash advances up to $250 through its Instant feature. A free tier exists alongside the paid Genius subscription ($14.99/month), which unlocks higher limits and financial advice from human advisors.

Advance amounts are determined algorithmically, meaning two users with similar income can receive very different limits. Albert provides minimal transparency about what drives those decisions. Gig workers with variable deposits frequently report being approved for amounts well below the $250 ceiling — sometimes as little as $25.

7. Klover

Klover advances up to $200 with no subscription fee — one of the few genuinely free options in the cash advance space. The app uses a points-based system where users earn advance eligibility by engaging with the app, watching ads, or completing surveys.

That engagement model is the trade-off. Getting the full $200 requires consistent app usage, and the points system can feel like a second job. Instant transfers cost up to $3.99; standard transfers are free but take one to two business days. Klover does accept gig income, making it one of the more accessible options for non-traditional earners. Users who want the same no-credit-check convenience without the data-sharing trade-off can explore other cash advance apps like Klover that charge subscription fees instead.

8. Cleo

Cleo pairs cash advances up to $250 with an AI chatbot that handles budgeting, savings goals, and spending analysis. The app’s personality-driven interface skews younger — think sarcastic money coach rather than corporate banking app.

Advances require the Cleo Plus ($5.99/month) or Cleo Builder ($14.99/month) subscription. There is no free advance tier. The $5.99 price point sits between Dave and Brigit, making it a mid-range option. Cleo accepts gig and freelance income through connected bank accounts, though approval amounts for irregular earners tend to start conservatively.

9. Payactiv

Payactiv takes a fundamentally different approach: earned wage access rather than an advance against future deposits. Users can access up to $500 of wages they’ve already worked for, with no interest, no credit check, and no subscription fee. The Consumer Financial Protection Bureau (CFPB) has issued guidance distinguishing earned wage access from traditional lending.

The limitation is structural. Payactiv only works if an employer has partnered with the platform. Individual users cannot sign up independently. Major employers including Walmart and Waffle House have enrolled, but coverage is far from universal. If your employer participates, Payactiv is arguably the best deal on this entire list.

10. Gerald

Gerald is the only app here that charges absolutely nothing — no subscription, no instant transfer fee, no tips. Advances up to $100 arrive with zero cost attached. Gerald accepts gig income, making it one of the most accessible options available.

The catch is indirect. To unlock a cash advance, users must first purchase a Gerald product (typically a small buy-now-pay-later item from partner merchants). That purchase activates advance eligibility. The $100 ceiling is also the lowest on this list, limiting Gerald to minor shortfalls rather than genuine emergencies. For users who need $50 or less — the same range FloatMe covers — Gerald delivers it for free.

How to Choose the Right FloatMe Alternative

The right app depends on three variables: how much cash is needed, how quickly it’s needed, and what type of income the user earns.

- Highest advance ceiling: EarnIn ($750) and Dave or MoneyLion ($500 each) lead the pack for users who need more than FloatMe’s $50.

- Lowest total cost: Gerald ($0), Chime SpotMe ($0), and Klover ($0 subscription) are the only truly free options. Payactiv is also free but requires employer enrollment.

- Gig workers and freelancers: Klover, Gerald, Albert, Cleo, and MoneyLion (via RoarMoney) all accept non-W-2 income. EarnIn, Brigit, Chime, and Payactiv do not.

- Fastest delivery: Chime SpotMe is instant at no cost. EarnIn, Dave, and MoneyLion offer paid express options under $10.

Stacking two apps — one free option for small shortfalls and one higher-limit option for real emergencies — is a practical strategy many users adopt. Gerald or Klover handles the $50 to $100 range at zero cost, while Dave or EarnIn covers larger gaps.

Frequently Asked Questions

What apps let you borrow more than FloatMe’s $50 limit?

Every app on this list offers a higher ceiling than FloatMe. EarnIn tops out at $750 per pay period. Dave and MoneyLion each offer up to $500. Brigit, Albert, and Cleo cap at $250. Even Gerald, the lowest on the list, matches FloatMe at $100 with zero fees attached.

Are there cash advance apps with no subscription fee?

EarnIn, Chime SpotMe, Klover, Payactiv, and Gerald all operate without a monthly subscription. EarnIn uses an optional tip model. Chime SpotMe is built into free Chime banking. Gerald monetizes through partner product purchases instead of direct fees.

Which apps like FloatMe work for gig workers?

Klover, Gerald, Cleo, Albert, and MoneyLion (through RoarMoney) accept non-W-2 income. Approval amounts for gig workers tend to start lower than for users with traditional direct deposits, but eligibility itself is not restricted. EarnIn, Brigit, Chime, and Payactiv require W-2 employment verification.

Do cash advance apps affect your credit score?

None of the ten apps listed here perform a hard credit inquiry during the application process. Cash advances from these apps are not reported to credit bureaus — meaning they won’t help build credit either, with the exception of Brigit and MoneyLion, which offer optional credit-builder features as separate products.

How fast can I get money from a FloatMe alternative?

Chime SpotMe delivers funds instantly at no cost. EarnIn’s Lightning Speed, Dave’s express, and MoneyLion’s instant transfer options deliver within minutes for fees ranging from $3 to $15. Free standard transfers across most apps take one to three business days.

Is it safe to use cash advance apps?

The apps listed here are licensed financial services providers, not payday lenders. EarnIn, Dave, Brigit, and Chime are regulated by state financial authorities and comply with federal consumer protection laws. The CFPB has published guidance on earned wage access products that applies to several of these apps. Always verify licensing through your state’s financial regulator before sharing bank credentials with any app.

Can I use more than one cash advance app at the same time?

Technically, yes. Each app evaluates eligibility independently based on the linked bank account. Many users maintain two or three apps for different scenarios — a free option like Gerald for small needs and a higher-limit option like Dave for larger shortfalls. Be aware that multiple apps debiting the same bank account on payday increases overdraft risk.

Making the Switch from FloatMe

FloatMe’s $50 cap, $3.99 subscription, and W-2-only eligibility make it one of the least competitive cash advance apps available. Every alternative reviewed here exceeds FloatMe on at least two of those three dimensions. EarnIn and Dave offer dramatically higher ceilings. Gerald and Chime SpotMe eliminate fees entirely. Klover and Cleo open the door for gig workers FloatMe turns away.

The effective cost of any cash advance app — subscription plus express fees, annualized — is almost always higher than a traditional personal loan or credit card. These apps are designed for short-term gaps, not ongoing borrowing. Used that way, the right alternative to FloatMe can cover a real emergency without the subscription overhead or the frustration of a $50 ceiling that doesn’t cover much of anything.