Afterpay, Klarna, and Sezzle are the strongest apps like Zip Pay available in 2026 — each offering interest-free installments with no monthly account fee, which is the most common reason shoppers start looking for a Zip Pay alternative in the first place. Zip Pay’s $6 monthly account-keeping charge applies even in months you don’t spend, and Zip Pay’s merchant network thins out considerably outside Australia.

Rejection is the other driver. Zip Pay’s approval process has tightened, and a denied application leaves shoppers needing a working split payment app fast — ideally one with a softer credit check or no credit check at all. Geography matters too. Zip Pay was built for the Australian market, and several of its closest competitors don’t operate there, while others do but under different names or product structures.

What follows cuts through that confusion directly. Each major buy now pay later alternative is benchmarked against Zip Pay’s actual features — spending limits, fees, repayment terms, country availability, and credit requirements — in a scannable comparison table, a full fee and credit-impact breakdown, and a short buyer-persona guide so the right deferred payment shopping app becomes obvious fast.

How Zip Pay Works (Your Comparison Baseline)

Zip Pay offers a revolving line of credit between $350 and $1,500 AUD, charges no interest, and collects a $6 monthly account-keeping fee — waived entirely if you clear your balance before the billing cycle closes. Repayments are fortnightly, and the product is built primarily for Australian consumers, with only limited merchant reach outside that market. Understanding this baseline makes every alternative easier to evaluate.

Zip Pay key features at a glance

| Feature | Detail |

|---|---|

| Credit limit | $350–$1,500 AUD |

| Interest | None |

| Account fee | $6/month (waived if balance is $0) |

| Repayment schedule | Fortnightly minimum payments |

| Primary availability | Australia (limited global reach) |

| Credit check | Soft check on application |

Zip Pay functions as a buy now pay later line of credit rather than a fixed installment loan — meaning the credit reloads as you repay, similar to a store card. That revolving structure distinguishes Zip Pay from most split payment apps, which lock repayments to a single purchase.

Who Zip Pay is best (and worst) for

Zip Pay suits Australian shoppers making mid-range purchases — clothing, homewares, or electronics under $1,500 — who prefer flexible deferred payment shopping over rigid four-installment schedules. The no-interest model keeps costs predictable, provided the balance clears monthly.

The friction points are real. The $6 fee accumulates even in months you don’t spend, effectively penalizing light or infrequent users. Outside Australia, Zip Pay’s merchant network thins considerably, and approval rates for first-time applicants can be stricter than competing interest-free installments platforms like Afterpay or Klarna.

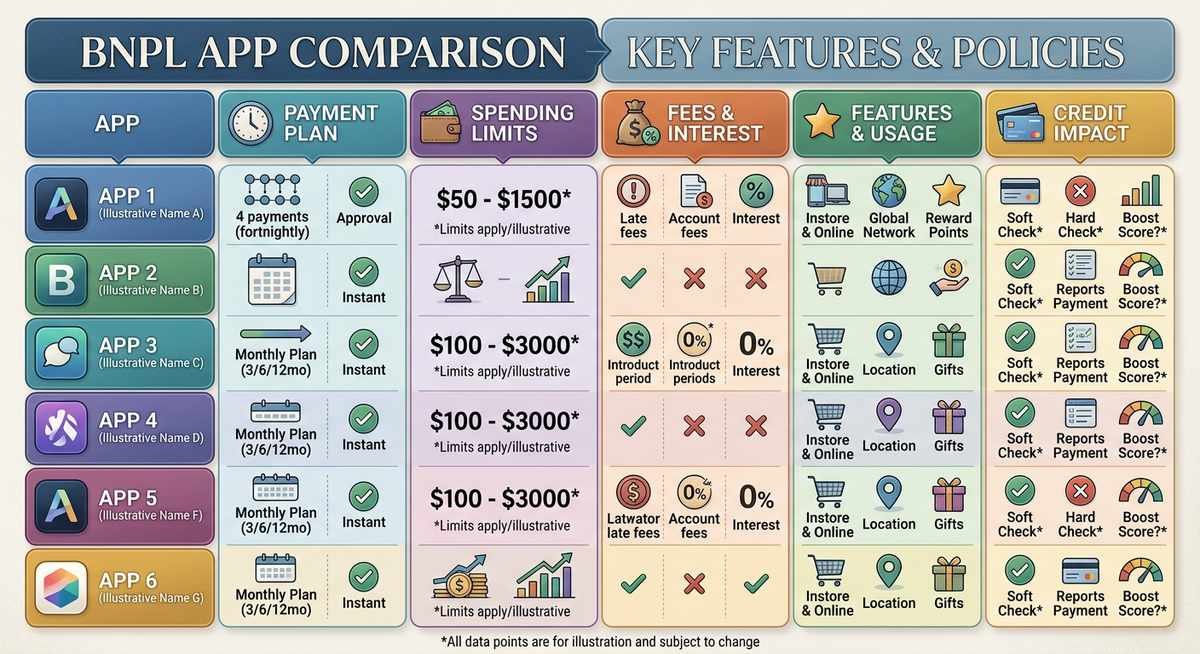

Top Apps Like Zip Pay Compared Side by Side

Afterpay is the closest like-for-like swap for Zip Pay in Australia, Klarna leads globally, Affirm wins for high-ticket purchases, and Sezzle stands out for credit-building in North America. The table below maps all six alternatives against Zip Pay across the five metrics that matter most — spending limits, fees, repayment structure, availability, and credit check requirements. According to Afterpay’s 2023 annual report, Afterpay processed over 24 million active customers globally, making it the largest BNPL platform by user count in the Australian market.

Comparison Table

| App | Available In | Spending Limit | Repayment Structure | Fees | Credit Check Required |

|---|---|---|---|---|---|

| Zip Pay (baseline) | Australia (primary) | $350–$1,500 | Fortnightly minimum repayments | $6/month account fee (waived if balance cleared) | Soft check |

| Afterpay | Australia, US, UK, NZ, CA | Up to $2,000 | 4 fortnightly installments | No account fee; late fees capped at $10 per installment | Soft check only |

| Klarna | 45+ countries incl. AU & US | Varies by product; up to several thousand | Pay in 4, Pay in 30 days, or financing | No account fee; late fees vary by country | Soft check (hard for financing) |

| Sezzle | US, Canada (not AU) | Up to $2,500 | 4 payments over 6 weeks | No interest; small rescheduling fee (~$5) | Soft check |

| Laybuy | Australia, NZ, UK | Up to $1,200 | 6 weekly installments | No interest; late fees up to $10 | Soft check |

| Paidy | Japan only | Varies by user | Pay next month or 3-month split | No interest on standard plan | No traditional credit check |

| Affirm | US (primary), CA | Up to $30,000 | 3–36 monthly installments | No late fees; APR 0–36% | Hard check for larger loans |

Afterpay

Afterpay is the most direct replacement for Zip Pay among Australian shoppers — same market, similar merchant network, and zero monthly account fee. Repayments split across four fortnightly installments, with late fees capped at $10 per missed payment and a maximum of $68 on any single order. The spending limit reaches up to $2,000, and approval requires only a soft credit check, making Afterpay accessible for most first-time buy now pay later users.

Klarna

Klarna’s real advantage is flexibility. Three distinct payment models — pay in 4, pay in 30 days, and longer-term financing — mean Klarna adapts to a $40 clothing purchase and a $1,500 appliance equally well. Available in over 45 countries including Australia (since 2020) and the United States, Klarna is the strongest global option among split payment apps. Standard plans use a soft credit check; financing tiers may trigger a hard inquiry.

Sezzle

Sezzle splits purchases into four interest-free installments over six weeks — structurally similar to Afterpay, but with one standout feature: an optional credit-reporting program called Sezzle Up that reports on-time payments to major credit bureaus. That makes Sezzle genuinely useful for shoppers trying to build credit while using deferred payment shopping. The catch is geography — Sezzle operates primarily in the US and Canada, with no meaningful Australian presence.

Affirm

Affirm targets a different buyer entirely. Repayment terms stretch from 3 to 36 months, spending limits can reach $30,000, and the APR is disclosed upfront — ranging from 0% to 36% depending on the merchant and the borrower’s profile. There are no late fees, which is a meaningful differentiator in the BNPL space. For high-ticket electronics, furniture, or medical expenses, Affirm’s transparent longer-term financing outperforms any pay-in-4 model — though larger loans do require a hard credit check. According to Affirm’s fiscal year 2024 shareholder letter, Affirm partnered with over 300,000 active merchants as of June 2024.

Fees and Credit Impact — The Full Transparency Breakdown

Zip Pay’s $6 monthly fee is the most expensive recurring charge among mainstream BNPL apps — Afterpay, Klarna, and Sezzle all charge zero account fees. Across the major split payment apps, the real cost differences come down to four variables: late fees, account-keeping fees, interest on financing tiers, and merchant surcharges that never appear in the app itself.

Fee Comparison Mini-Table

| App | Late Fee | Account / Monthly Fee | Interest | Hidden Surcharges |

|---|---|---|---|---|

| Zip Pay | $5 per missed payment | $6/month (waived if balance cleared) | None | Possible merchant surcharge |

| Afterpay | $10 per missed payment (capped at 25% of order value) | None | None | Rare merchant surcharge |

| Klarna (Pay in 4) | Up to $7 per missed payment | None | None (financing tier: 0–29.99% APR) | None standard |

| Sezzle | $10 rescheduling fee | None (Sezzle Premium: $7.99/month optional) | None | None standard |

| Affirm | None | None | 0–36% APR depending on loan term | None |

On merchant surcharges: some retailers pass BNPL processing fees — typically 2–6% of the transaction — directly to customers at checkout. This isn’t charged by the app; the retailer applies the surcharge. Always check the final checkout total before confirming a deferred payment shopping order, particularly with smaller independent merchants.

How Each App Affects Your Credit Score

A soft credit check pulls your credit file for assessment without leaving a visible mark — Afterpay, Klarna’s pay-in-4, and Sezzle all use soft checks at approval. A hard credit check, used by Affirm for larger financing amounts, does appear on your credit report and can temporarily lower your score by a few points.

Reporting on-time payments is a separate question entirely. Afterpay and Klarna’s pay-in-4 do not report positive payment history to any credit bureau, meaning responsible use of those interest-free installments builds zero credit history. Sezzle offers an opt-in credit-reporting feature through Sezzle Premium that reports payments to all three major US bureaus. Affirm reports all loans — including on-time payments — directly to Experian, making Affirm the strongest credit-building tool among mainstream BNPL options.

Missed payments are a different story across every platform. Afterpay can refer overdue accounts to collections. Klarna and Zip Pay report delinquencies to credit bureaus even when neither reports positive behavior. According to the Consumer Financial Protection Bureau (2022), BNPL delinquency reporting practices remain inconsistent across providers — a known gap that regulators are actively reviewing. Treat any deferred payment shopping commitment as a real debt obligation, regardless of how frictionless the checkout feels.

Australia vs. US vs. Global — Which Apps Like Zip Pay Actually Work Where You Are

Geographic availability is the single most important factor most BNPL comparison articles ignore. Afterpay works in Australia and the US but with different fee structures; Affirm is effectively US-only; Klarna operates in 45+ countries. Knowing which split payment apps are live in your region saves you from downloading something that won’t work at checkout.

Apps Available in Australia

Afterpay is the natural Zip Pay replacement for Australian shoppers — Afterpay launched in Australia in 2014 and maintains the country’s largest BNPL merchant network. Klarna entered the Australian market in 2020 and now supports buy now pay later across hundreds of local retailers. Laybuy, founded in New Zealand, operates across both Australia and New Zealand with a six-weekly repayment model.

Sezzle and Affirm are not meaningfully available in Australia. Both platforms are built around US financial infrastructure, and neither has launched a functional Australian product. Attempting to use either from an Australian billing address will typically result in a declined application.

Apps Available in the US

Affirm, Klarna, Sezzle, and Afterpay all operate fully in the United States. Afterpay’s US version runs through Square’s payment infrastructure following Square’s 2021 acquisition, which means Afterpay’s merchant integrations and spending limits differ slightly from the Australian product. Zip Pay’s US equivalent is a rebranded product simply called “Zip” — but the deferred payment shopping structure, fee model, and credit terms are materially different from what Australian users recognize.

US shoppers have the broadest range of interest-free installments options globally. According to Affirm’s fiscal year 2024 shareholder letter, Affirm alone partnered with over 300,000 active merchants as of June 2024.

Truly Global Options

Klarna is the most internationally versatile BNPL platform available, operating across North America, Europe, Australia, and parts of Asia. For shoppers outside Australia and the US, regional alternatives fill the gap: Paidy dominates the Japanese deferred payment shopping market, while Scalapay serves Italy, Germany, France, and other European markets with a pay-in-3 model. No single app covers every country, but Klarna comes closest for travelers and international shoppers who need one consistent platform. According to Klarna’s 2023 annual report, Klarna served over 150 million active consumers across 45 countries.

| App | Australia | United States | Europe | Other Regions |

|---|---|---|---|---|

| Zip Pay | Yes Native | Partial: Rebranded “Zip” (different product) | No | Limited |

| Afterpay | Yes Native | Yes (via Square) | Yes Select markets | NZ, CA |

| Klarna | Yes Since 2020 | Yes | Yes 20+ countries | 45+ total |

| Sezzle | No | Yes | No | Canada only |

| Affirm | No | Yes | No | CA (limited) |

| Laybuy | Yes | No | Yes UK | NZ native |

| Paidy | No | No | No | Japan only |

Which App Is Right for You

The best Zip Pay alternative depends on how you actually shop — where, how much, and whether credit-building matters. Picking the wrong app means either getting declined at checkout or paying fees you could have avoided entirely.

Best for In-Store Installments

Afterpay and Klarna both offer virtual cards that work at physical retailers through Apple Pay and Google Pay — making them the strongest apps like Zip Pay you can use in store with installments. Afterpay’s in-store network covers major Australian chains including Kmart, Big W, and Cotton On. Klarna’s in-store virtual card works at any retailer that accepts contactless payments, giving Klarna a broader physical footprint than Afterpay in the US market.

Best for Paying Bills and Rent

Standard BNPL apps like Afterpay and Klarna do not support bill payments or rent directly — they require a merchant integration at checkout. Deferit fills this gap in Australia, allowing users to pay household bills (electricity, internet, insurance) in four fortnightly installments with no interest and no credit check. For rent specifically, services like Flex in the US split monthly rent into smaller payments. Neither Zip Pay nor standard split payment apps were designed for recurring bills, so dedicated bill-payment BNPL tools are the practical answer.

Best No Credit Check Options

Afterpay and Klarna’s pay-in-4 use only soft credit checks — no impact on your credit score and no hard inquiry visible to lenders. For shoppers specifically seeking apps like Zip Pay with no credit check in Australia, Afterpay remains the safest bet since approval rates for first-time users are higher than Zip Pay’s. Deferit also runs no traditional credit check for bill payments. In the US, Sezzle’s soft check approval and low entry requirements make Sezzle accessible for most applicants regardless of credit history.

Best for Groceries and Everyday Spending

Klarna’s virtual card works at grocery stores that accept contactless payments, making Klarna the most practical BNPL option for groceries. Afterpay’s in-store feature also works at select grocery retailers in Australia. For Amazon purchases specifically, Affirm offers a direct integration — shoppers can select Affirm at Amazon checkout to split the total into monthly payments, which no other major BNPL app offers natively on Amazon.

Frequently Asked Questions

What is the best alternative to Zip Pay for online shopping?

Afterpay is the strongest like-for-like swap for Australian online shoppers — no monthly account fee, fortnightly pay-in-4 structure, and a merchant network that rivals or exceeds Zip Pay’s. For international online shopping, Klarna’s availability across 45+ countries makes Klarna the more versatile pick.

Does Zip Pay work in the US, or do I need a different app?

The Zip Pay product Australian users know is not directly available in the US. Zip relaunched under the “Zip” brand in the US market, but the product structure — fees, limits, and repayment terms — differs materially from the Australian version. US shoppers are better served by Affirm, Klarna, or Sezzle.

Which buy now pay later apps don’t do a credit check?

Afterpay and Klarna’s pay-in-4 option both use soft credit checks only, meaning no impact on your credit score at application. Neither Afterpay nor Klarna reports on-time payments to credit bureaus, so both are low-risk but offer no credit-building benefit. Paidy requires no traditional credit check at all, but Paidy is only available in Japan.

Can I use multiple buy now, pay later apps at the same time?

Yes, you can hold accounts across multiple BNPL apps simultaneously — Afterpay, Klarna, and Zip Pay can all be active at once. The practical risk is overextension. Stacking deferred payment shopping across three or four apps makes repayment tracking difficult, and missed payments on any platform can trigger late fees or credit bureau reports depending on the provider.

Is Zip Pay legit?

Zip Pay is a legitimate, publicly listed financial services company (ASX: ZIP) regulated by the Australian Securities and Investments Commission (ASIC). Zip Pay has operated since 2013 and holds an Australian Credit Licence. The $6 monthly account fee and soft credit check on application are standard practices — Zip Pay is not a scam, though the recurring fee structure makes Zip Pay more expensive than fee-free alternatives like Afterpay for light users.

What is the difference between Zip Pay and Afterpay?

Zip Pay offers a revolving credit line of $350-$1,500 AUD with fortnightly minimum payments and a $6 monthly fee, while Afterpay splits each purchase into exactly four fortnightly installments with no account fee. The Zip Pay vs Afterpay decision typically comes down to flexibility versus simplicity — Zip Pay’s revolving credit suits ongoing spending, while Afterpay’s fixed four-payment structure is easier to manage for one-off purchases.

How does Zip Pay compare to Klarna?

Klarna offers three payment models (pay in 4, pay in 30 days, and longer-term financing) across 45+ countries, while Zip Pay’s revolving credit operates primarily in Australia. The Zip Pay vs Klarna comparison favors Klarna for international availability and product flexibility, but Zip Pay’s higher credit limit ($1,500 vs Klarna’s variable limits) can suit Australian shoppers making larger purchases within a single retailer.

Which BNPL apps offer virtual cards for in-store shopping?

Afterpay, Klarna, and Zip all offer virtual cards that integrate with Apple Pay or Google Pay for in-store purchases. Afterpay’s virtual card works at any retailer accepting contactless payments in Australia, the US, and the UK. Klarna’s virtual card functions similarly across supported markets. These virtual card BNPL apps effectively let you use buy now pay later at any physical store, not just partnered merchants.

Wrapping Up

The right buy now pay later app comes down to three variables: where you live, your credit situation, and how much you need to spend. For Australian shoppers replacing Zip Pay, Afterpay is the default swap — no monthly account fee, a wider merchant network, and a soft credit check that keeps approval barriers low. Globally, Klarna’s presence across 45+ countries makes Klarna the most versatile split payment app available today.

One pattern stands out across every alternative: the BNPL market is consolidating around zero-fee, pay-in-4 models. Zip Pay’s $6 monthly account fee and revolving credit structure are increasingly outliers in a space moving toward simpler, fixed-installment products. Shoppers who switch now are unlikely to switch back — the fee-free alternatives simply offer more for less. Start small, track repayments like any real debt, and verify eligibility directly on the app’s official site before applying.