Accredited Debt Relief is a legitimate, BBB-accredited debt settlement company founded in 2011 in San Diego — but “legitimate” and “right for your situation” are different claims entirely. The company holds an A+ Better Business Bureau rating, maintains membership in the American Fair Credit Council (AFCC), and complies with Federal Trade Commission rules that prohibit collecting fees before a creditor settlement agreement is reached.

None of that changes the mechanics of what enrollment actually involves. You stop paying creditors. Your credit score drops — often by 100 points or more. Fees run 15%–25% of enrolled debt. The IRS may treat forgiven balances as taxable income. Any honest review that skips these realities is doing readers a disservice.

What follows is a forensic look at the company’s credentials, what real users report across Reddit and Trustpilot, how the numbers actually work, and when this legitimate program makes financial sense — or doesn’t.

What Is Accredited Debt Relief and How Does It Work?

Accredited Debt Relief is a debt settlement brokerage that connects consumers carrying $10,000 or more in unsecured debt to a network of third-party settlement attorneys and negotiators. The company does not negotiate directly, does not lend money, and is not a nonprofit credit counseling agency — distinctions that matter when comparing options.

Company Background and Credentials

Founded in 2011 and headquartered in San Diego, California, the company operates as a legitimate business registered with state financial regulators across its service areas. The American Fair Credit Council (AFCC) is the debt settlement industry’s primary accrediting organization, and Accredited Debt Relief has maintained continuous membership — which requires compliance with ethical standards governing fee transparency and client disclosures.

This is a real company with a verifiable physical address, state registrations, and a 14-year operating history. Consumers can independently confirm its standing through the AFCC’s public member directory and their state attorney general’s financial services division.

How the Program Works Step by Step

- Free consultation: A representative reviews your total unsecured debt, income, and financial hardship to determine eligibility. The minimum debt threshold is typically $10,000.

- Dedicated savings account: You open an FDIC-insured savings account in your own name and begin depositing a fixed monthly amount. Payments to enrolled creditors stop — this creates the leverage needed for negotiation and is also what triggers credit damage.

- Account-by-account negotiation: Once sufficient funds accumulate, settlement attorneys approach individual creditors to negotiate reduced payoff amounts, typically targeting 40%–60% of the original balance.

- Program completion: Settled accounts are closed, fees are collected per resolved account, and the program ends. Total duration runs 24–48 months depending on enrolled debt volume.

| Program Detail | Specification |

|---|---|

| Founded | 2011, San Diego, CA |

| Debt types accepted | Credit cards, medical bills, personal loans, some private student loans |

| Minimum enrolled debt | $10,000 |

| Program length | 24–48 months |

| Fee range | 15%–25% of enrolled debt |

| AFCC member | Yes |

| BBB rating | A+ |

Accredited Debt Relief Reviews: BBB, Trustpilot, Reddit, and More

The company’s review profile splits sharply depending on which platform you check — a 4.9-star Trustpilot rating from more than 10,000 reviews, an A+ BBB grade, and a 2.3-star Yelp score. That dramatic split reflects both genuine client satisfaction and the inherent frustrations of the debt settlement process.

BBB Rating and Accreditation Status

Accredited Debt Relief holds an A+ rating with the Better Business Bureau and has been BBB-accredited since its founding. The A+ grade reflects the complaint-resolution track record, not customer satisfaction — a distinction the BBB itself makes clear. Ratings are based on response to complaints, business transparency, and licensing, not average review scores.

The BBB profile does show complaints, mostly centered on communication gaps during the negotiation phase and timelines that exceeded initial estimates. The company has responded to these complaints publicly, which is part of why the rating remains high despite periodic customer frustration.

Trustpilot and Google Reviews

On Trustpilot, the company carries a 4.9 out of 5.0 rating across more than 10,000 reviews — an unusually high volume for the debt settlement industry. Positive Accredited Debt Relief reviews on Trustpilot consistently cite responsive customer service and successful debt reductions. The most frequent praise mentions specific staff members by name, which typically signals genuine client experiences rather than templated responses.

Accredited Debt Relief Google reviews are harder to aggregate because the company operates primarily through phone consultations rather than physical locations. Available Google ratings trend positive and largely mirror Trustpilot patterns, though with a smaller sample size.

Yelp tells a different story. The company holds a 2.3-star rating from roughly 35 Yelp reviews, with complaints focusing on extended timelines, communication breakdowns during negotiation, and confusion about the fee structure. Yelp’s smaller sample and the platform’s tendency to attract dissatisfied customers may explain part of the gap, but the complaints themselves describe real friction points that prospective clients should understand.

Reddit Reviews, Complaints, and Real User Experiences

Reddit threads — particularly in r/debtfree, r/personalfinance, and r/debt — provide the most unfiltered assessments available. The consensus across multiple Accredited Debt Relief Reddit threads: the company is legit, but the credit score damage during enrollment is more severe than sales representatives initially suggest.

Common complaints on Reddit include surprise at the credit impact, frustration with the pace of settlements, and discovering the tax consequences of forgiven debt mid-program. Users who completed the full program generally report net-positive outcomes. Those who dropped out early describe the experience negatively — often because they exited before any settlements were reached but after their credit had already taken a hit.

Consumer Reports does not currently publish a dedicated review of this company. Reddit users searching for Accredited Debt Relief reviews from Consumer Reports are generally directed to the Consumer Financial Protection Bureau’s complaint database, which tracks formal complaints against financial services companies including debt settlement providers.

Accredited Debt Relief Pros and Cons

The program works well for a specific profile: consumers carrying $15,000 or more in unsecured debt who have already missed payments and exhausted lower-impact options like credit counseling. For everyone else, the tradeoffs tilt unfavorable.

| Pros | Cons |

|---|---|

| A+ BBB rating and AFCC membership — verified, independently confirmable credentials | Credit score drops 100+ points during the first 3–6 months of enrollment |

| No upfront fees — payment only after each creditor settlement agreement is reached | Fees of 15%–25% significantly reduce net savings after settlement |

| Free initial consultation with no enrollment obligation | Forgiven debt may generate a taxable event (IRS 1099-C) |

| Potential to reduce total unsecured debt by 30%–50% before fees | Program duration of 24–48 months with no guaranteed timeline |

| 4.9 stars on Trustpilot from 10,000+ verified reviews | Creditors can sue during the payment-stoppage period |

| Dedicated FDIC-insured savings account held in your name | Not available in all states; results vary by creditor willingness to negotiate |

Whether Accredited Debt Relief is a good company for your situation depends on one calculation: does the potential debt reduction outweigh the combined costs of fees, credit damage, possible tax liability, and lawsuit risk? For someone already drowning in unsecured debt with no realistic path to repay in full, those tradeoffs may be worth accepting. For someone who can still make minimum payments and maintain decent credit, cheaper alternatives exist.

Fees, Costs, and the Tax Surprise

The company charges between 15% and 25% of enrolled debt as its fee, collected only after each creditor settlement agreement is reached — never upfront. That post-settlement timing is legally mandated by the Federal Trade Commission’s Telemarketing Sales Rule (amended 2010), which prohibits any debt settlement company from collecting fees before delivering results.

Fee Structure Breakdown

Fees accumulate per settled account, not as a lump sum at program end. A concrete example: $30,000 in enrolled unsecured debt settled at 50 cents on the dollar means $15,000 paid to creditors. Add a 25% fee on the original enrolled amount ($7,500) and total outlay reaches $22,500 — a genuine saving over the original $30,000, but meaningfully less than the “settle for half” headline suggests.

| Enrolled Debt | Settlement Rate | Paid to Creditors | Fee (25%) | Total Cost | Net Savings |

|---|---|---|---|---|---|

| $20,000 | 50% | $10,000 | $5,000 | $15,000 | $5,000 |

| $30,000 | 50% | $15,000 | $7,500 | $22,500 | $7,500 |

| $50,000 | 40% | $20,000 | $12,500 | $32,500 | $17,500 |

One clarification that trips people up: Accredited Debt Relief is not a loan program. No money is lent to you, and no new debt is created. The “is Accredited Debt Relief loan legit?” question appears frequently in search data, but the company provides unsecured debt negotiation services — not lending. Your dedicated savings account holds your own money throughout the program.

The 1099-C Tax Consequence

Forgiven debt is taxable income. Under IRS rules, any creditor that forgives more than $600 must issue a 1099-C form, and that forgiven amount gets added to your ordinary taxable income for the year.

On the $30,000 example above, the $15,000 forgiven balance could generate a tax bill of $1,800–$3,300 depending on your federal bracket. These costs don’t appear in any program’s advertised savings figures.

One legitimate offset exists: IRS Form 982, the insolvency exclusion. If your total liabilities exceeded your total assets when the debt was forgiven, you may qualify to exclude some or all of that forgiven amount from taxable income. Qualifying requires documentation and a working knowledge of IRS insolvency definitions. According to the IRS, insolvency is determined immediately before the cancellation of debt — consult a tax professional before enrolling, not after your first settlement arrives.

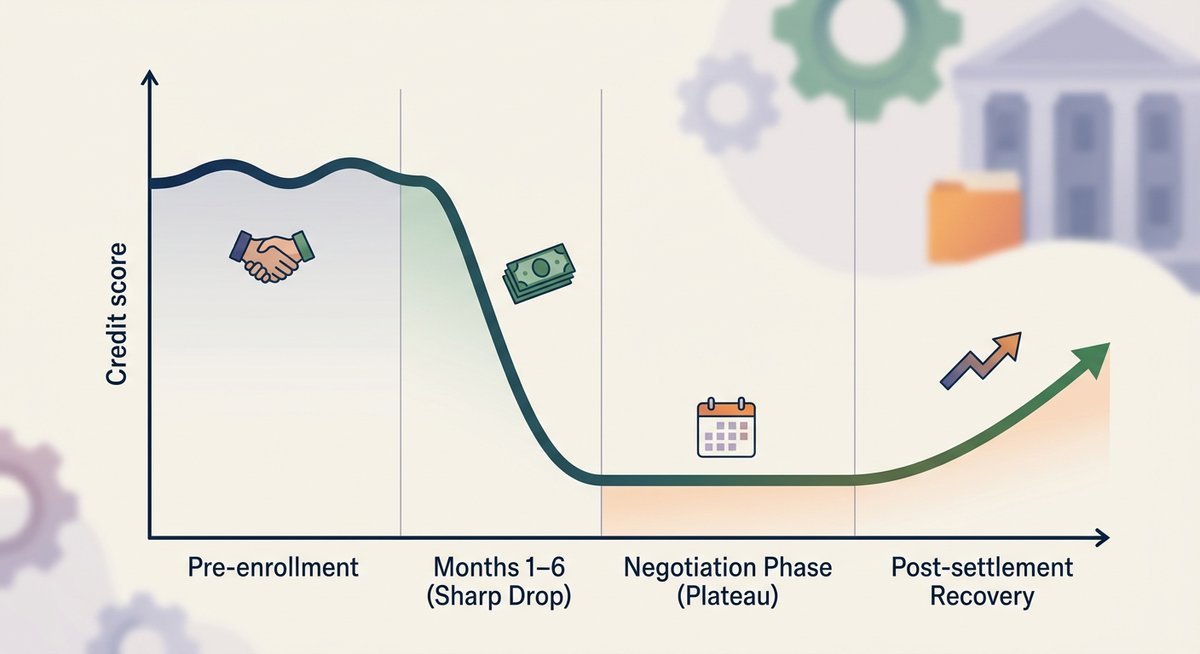

How Enrollment Affects Your Credit Score

Enrolling in the program will damage your credit score — typically by 100 points or more within the first three to six months. That damage is structural, not accidental: the entire strategy depends on stopping payments so accounts become delinquent and negotiable.

The Credit Damage Timeline

| Stage | Timeframe | Credit Impact |

|---|---|---|

| Payments stop | Month 1–2 | First missed-payment marks appear; score begins declining |

| Serious delinquency | Month 3–6 | Score may drop 100+ points; charge-offs possible after 180 days |

| Active negotiation | Month 6–36 | Score remains suppressed; no new negatives if no new debt is taken on |

| First creditor settlement agreement reached | Varies | Account marked “settled for less” — negative but stops active delinquency reporting |

| Post-program recovery | 12–24 months after last settlement | Gradual score improvement as negative marks age |

Under the Fair Credit Reporting Act, delinquencies and “settled for less than full balance” notations can remain on a credit report for seven years from the original delinquency date. The meaningful shift is that active negative reporting stops once each account is resolved. Clients who avoid taking on new debt typically see measurable score recovery 12–24 months after their first settlement clears.

Lawsuit Risk During the Program

One risk that most reviews of Accredited Debt Relief skip entirely: creditors can sue you during the payment-stoppage period. When you stop paying, creditors retain every legal right to pursue collection through the courts. Credit card companies in particular may file suit after 90–180 days of non-payment, especially on larger balances.

The company’s settlement attorneys can sometimes negotiate with creditors who have filed suit, but a judgment against you adds a separate negative mark and potentially allows wage garnishment depending on your state’s laws. This risk is highest in the early months before settlements begin, when accounts are most delinquent and no resolution has been offered.

Is It a Scam? How to Verify Any Debt Relief Company

Accredited Debt Relief is not a scam — it passes every standard legitimacy check available to consumers. But the debt relief industry broadly harbors predatory operators, and knowing how to spot a real company versus a fake one protects you regardless of which provider you evaluate.

Run through this four-step credential verification before enrolling with any BBB-accredited debt relief firm or any company claiming that status:

- Search the AFCC’s public member directory to confirm current membership.

- Check the company’s BBB profile for both the letter grade and complaint history — a high rating with dozens of unresolved complaints tells a different story than the grade alone.

- Look up state licensing through your state’s financial regulatory agency or attorney general website; an unlicensed operator is an immediate disqualifier.

- Search the CFPB complaint database for the company name and read the complaint narratives, not just the count.

Universal red flags that signal a debt relief scam regardless of the company: demanding upfront fees before any service is rendered (a direct FTC violation), guaranteeing specific settlement percentages, pressuring you to stop communicating with creditors without written explanation, providing only a P.O. box address, and refusing to produce a written contract before enrollment.

Accredited Debt Relief vs. Your Alternatives

Debt settlement is one option among five realistic paths for managing unsecured debt, each with different costs, credit consequences, and eligibility thresholds.

| Option | Best For | Typical Cost | Credit Impact | Timeline |

|---|---|---|---|---|

| Accredited Debt Relief (settlement) | $15K+ unsecured debt, already missing payments | 15%–25% of enrolled debt + potential tax bill | Severe (100+ point drop) | 24–48 months |

| Nonprofit credit counseling (DMP) | Can afford reduced monthly payments, want to protect credit | $25–$75/month setup and maintenance | Minimal to none | 36–60 months |

| Debt consolidation loan | Good credit score, multiple high-interest balances | Loan interest (varies by creditworthiness) | Temporary small dip | 24–60 months |

| DIY settlement | Financially literate, lump sum available, few accounts | $0 in professional fees | Moderate to severe | Varies widely |

| Chapter 7 bankruptcy | No realistic path to repayment | $1,500–$3,500 in attorney fees | Severe (remains on report 7–10 years) | 3–6 months |

Accredited Debt Relief makes the most financial sense for consumers who have already exhausted credit counseling and balance transfer options, carry substantial unsecured debt, and need structured support that DIY negotiation cannot provide. For debts under $10,000 or situations where you can still make minimum payments, a nonprofit debt management plan through the National Foundation for Credit Counseling typically delivers better outcomes with far less collateral damage.

Frequently Asked Questions

Is Accredited Debt Relief a real company?

Yes. It is a real, registered company headquartered in San Diego, California, founded in 2011. The business holds an A+ BBB rating, AFCC membership, and state registrations that can be independently verified through public regulatory databases and the BBB’s online profile.

Is accrediteddebtrelief.com a legitimate website?

Yes. The domain accrediteddebtrelief.com is the official website, verified through the company’s BBB profile and AFCC listing. Always confirm you are on the correct URL before submitting personal financial information — the official domain uses no hyphens or additional words.

Does Accredited Debt Relief hurt your credit?

Yes. Enrollment requires stopping payments to creditors, which triggers delinquency reports that typically lower scores by 100 or more points within 3–6 months. Under the Fair Credit Reporting Act, those marks can remain on your report for seven years from the original delinquency date.

Is Accredited Debt Relief a loan?

No. The company provides debt negotiation services, not loans. No money is lent, and no new debt is created during the program. Negotiators work with existing creditors to accept reduced lump-sum payments from savings you accumulate in a dedicated FDIC-insured account.

What is the BBB rating for Accredited Debt Relief?

The company holds an A+ rating with the Better Business Bureau and has been BBB-accredited since its founding. The rating reflects complaint-resolution practices and business transparency, not average customer satisfaction scores.

Is Debt Aid Consulting International legit?

Debt Aid Consulting International is a separate company entirely. Before enrolling with any debt settlement provider, independently verify its BBB status, AFCC membership, state licensing, and CFPB complaint history using the four-step verification checklist above. Companies without verifiable credentials in all four areas should be treated with caution.

Is using Accredited Debt Relief worth it?

For consumers carrying $15,000 or more in unsecured debt who have already missed payments and exhausted lower-impact options, the program can reduce total debt obligations meaningfully. It is generally not worth it for people who can still make minimum payments, carry debts under $10,000, or cannot absorb 24–48 months of serious credit score damage.

How long does the program take?

Most clients complete the program in 24–48 months, depending on total enrolled debt and monthly deposit amounts. Larger balances with multiple creditors extend the timeline. No legitimate debt settlement company can guarantee a specific completion date because outcomes depend on individual creditor willingness to negotiate.

Can creditors sue you while enrolled in debt settlement?

Yes. Creditors retain the legal right to pursue collection through courts during the payment-stoppage period. Some creditors file suit after 90–180 days of non-payment, particularly on larger balances. While settlement attorneys can sometimes negotiate after a suit is filed, a judgment could result in wage garnishment depending on state law.

Conclusion

Accredited Debt Relief is a legitimate and reliable company with verifiable credentials: an A+ BBB rating, AFCC membership, FTC compliance, and a 14-year operating history. Real or fake is not the right question — this is definitively a real company with genuine credentials. The harder question is whether its program fits your specific financial situation.

The math demands honesty. Fees of 15%–25%, a credit score that drops 100+ points in the early months, potential IRS tax liability on forgiven debt above $600, and the risk of creditor lawsuits during the program are all real costs that make debt settlement unsuitable for everyone. For consumers already deep in unsecured debt with no viable path to repay in full, those costs may still represent the least-bad option on the table.

Before signing anything, take the free consultation — it carries no obligation. Then compare at least one alternative. A nonprofit credit counselor can assess whether a debt management plan would address your situation without the credit destruction that debt settlement requires.